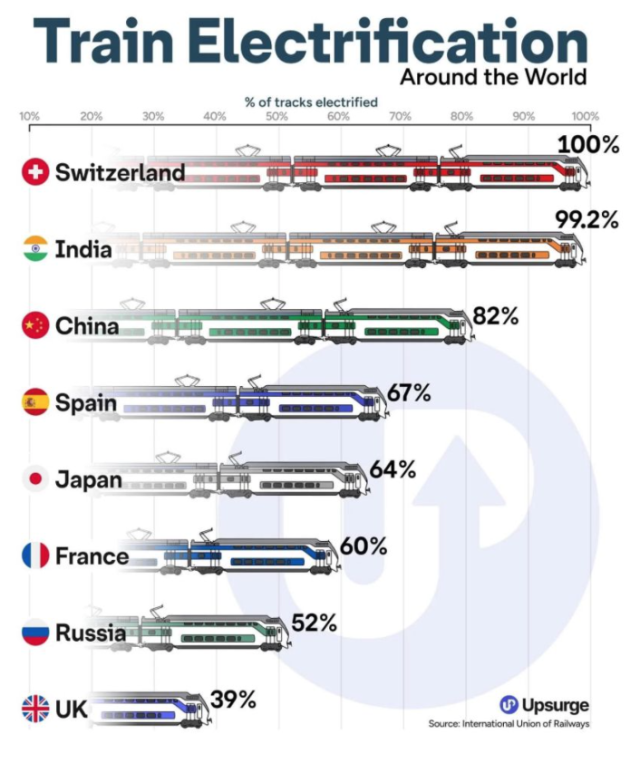

The UK’s relatively low level of rail electrification—39% compared to countries like Switzerland (100%) or India (99.2%) as shown below is they say the result of historical “stop-start” investment cycles and complex privatised structures.

Why UK Electrification is Lagging

Several factors have historically hindered the expansion of the electrified network:

-

“Stop-Start” Investment: Unlike Scotland’s rolling programme, the wider UK has suffered from fluctuating investment, which erodes industry confidence and inflates costs because skills and equipment are not maintained between projects.

-

Historical Success of Diesel: The unprecedented success of the “Intercity 125” (Class 43) diesel fleets in the late 20th century effectively stalled long-distance electrification projects as they provided a high-quality alternative to electric traction.

-

Fragmentation: Following privatisation in 1993, the lack of a single “whole-system” organisation made the financial case for electrification harder to justify, leading to a large-scale procurement of diesel trains instead.

The ROSCO Dividend Controversy

The role of Rolling Stock Operating Companies (ROSCOs) has come under intense scrutiny recently:

-

Record Dividends: In the 2022-23 financial year, ROSCOs actually paid out £409.7 million in dividends—significantly higher than the £275 million mentioned—representing a tripling of profits from the previous year.

-

High Lease Costs: While the rest of the railway faced budget cuts and salary freezes, ROSCO profit margins rose to 41.6%, with taxpayers continuing to provide high subsidies.

-

There is no doubt it has had an impact on investment: Critics argue these billions in dividends disappear into parent companies (often foreign pension funds) rather than being reinvested into infrastructure like electrification.

What Great British Railways (GBR) Plans to Do

Legislation introduced in late 2025 has paved the way for Great British Railways (GBR) to act as the “guiding mind” for the network, with full establishment expected by the end of 2027. Its goals include:

| GBR Strategy Area | Planned Improvements |

| Unified Strategy | Integrating track and train operations to allow for “whole-system” decision-making on electrification. |

| Long-Term Planning | Implementing 30-year strategic plans and five-year funding cycles to end the “stop-start” investment cycle. |

| Discontinuous Electrification | Utilising a £2.5 billion commitment (from late 2025) to focus on “bridging gaps” using battery-electric hybrid trains where full overhead wiring is too costly. |

| Infill Projects | Prioritising smaller “infill” schemes to enable 95% of rail freight to be hauled by electric power. |

In the immediate future (2026), major projects like the South Wales Metro (electrifying 170km) and the Transpennine Route Upgrade are core priorities to demonstrate that the new structure can deliver tangible progress.