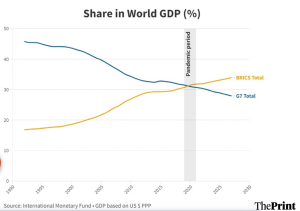

With the increasing easternisation of the world economy particularly around trade with China, as clearly evident by the BRICs combined GDP being bigger than G7 now, a discourse on alternative currencies for world trade is being opening discussed.

There are also economic sanctions considerations as well but a number of pull and push factors will mean at the mid-August annual Leaders meeting of BRICS Summit Conference, the new BRICS+ currency will announced but not probably be available in the form of paper notes for everyday transactions. It will be a digital currency on a permissioned ledger maintained by a new BRICS+ financial institutions with encrypted message traffic to record payments due or owing by participating parties. Though importantly it is proposed not to be decentralised, as its not maintained on a blockchain and not open to all parties without approval. So clearly a case needs to be made for the adoption fully blockchain technology to BRICs digital currency.

In the traditional financial system, many activities require multiple intermediaries: Banks maintain custody of funds, manage the process of lending and borrowing, and facilitate the transfer and settlement of money between accounts using intrabank and interbank systems. Brokerage services receive and fill orders to buy or sell securities with the help of other institutions that serve as market makers. Credit Suisse and Citadel Securities are some of the market makers that help create liquidity in the market by buying and selling securities within their own accounts.

Decentralised finance known as DeFi provides similar disintermediation services, making most financial activities possible through peer-to-peer networks through blockchain technology. DeFi disintermediation provides financial alternatives to individuals who might not use the traditional banking system. Further, DeFi solutions also offer efficient access to capital and interest earnings while offering privacy, control over custody of funds, and censorship resistance: Blockchain networks do not have a central authority or gatekeeper that prevents anyone from participating in the network, as long as participants follow the network’s rules, or an authority that changes or removes transactions on the network. Because of the immutable nature of blockchains, participants also cannot change or remove transactions. DeFi, in general, offers a new alternative source for financial services. Best example of Defi working for those who do not use the traditional banking system using blockchain technology is remittance flows from migrants from the developed world to the developing world.

Blockchain-based remittance services provide a novel and inventive method of sending and receiving funds across borders. They provide various advantages over traditional remittance services, such as faster and more secure payment processing, lower transaction fees, and enhanced transparency and accountability. As a result fintech industries have moved into this global market, with recent for example Coinbase partnering with remittance company Remitly to let crypto recipients in Mexico cash out digital currencies at over 37,000 retail stores. Coinbase will charge a minimal fee that is cheaper than traditional cross-border payment solutions. So as blockchain technology evolves and matures, we should expect to see increased use and innovation in this critical field.

Furthermore Web 3.0, the next evolution of the internet and distributed networks, plays an important role in DeFi. Whereas Web 2.0 is dominated by a handful of organisations, such as Google and Facebook, that act as intermediaries, Web 3.0 enables users to interact via peer-to-peer networks. Additionally, while major players in Web 2.0 offer their services in exchange for ownership of users’ personal data, which they can then sell, DeFi exchanges allow participants to maintain ownership of their personal data. Data ownership provides individuals control over how their personal data is used or not used by outside parties.